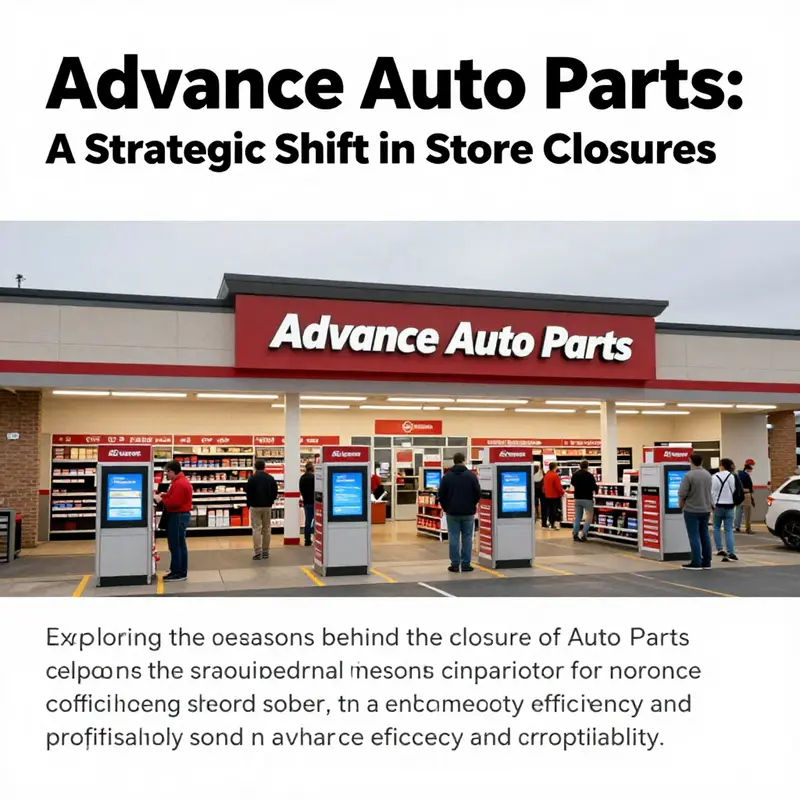

The decision by Advance Auto Parts to close several of its stores marks a critical moment in the retail landscape. This move isn’t merely a reaction to declining sales but rather part of a broader strategy aimed at optimizing operations, enhancing profitability, and ensuring long-term viability. Business owners should recognize that these closures reflect a decisive shift in focus towards operational efficiency, core business performance, and a response to evolving market demands. This article will delve into three key aspects of Advance Auto Parts’ strategy: the optimization of store networks for efficiency, the emphasis on core operations to drive profitability, and the adaptation to changing market demands that necessitate these closures.

Lean by Design: The Strategic Rationale Behind Store Closures at Advance Auto Parts

In the aftermarket landscape, where consumer preferences shift with the ease of online access and the tempo of everyday life, a strategic decision to close stores often signals a deeper transformation rather than a simple contraction. For Advance Auto Parts, the closures are not random exits but a deliberate reassembly of a sprawling network into a more focused, efficient engine. The narrative behind the store closures unfolds in several interlocking movements: a measured pruning of underperforming locations, a deliberate refocusing on core retail operations, and an adaptation to the changing rhythms of how people buy auto parts. Taken together, these moves are designed to convert a large, diffuse footprint into a leaner, more resilient platform capable of sustained profitability in a market marked by online competition, inflation, and evolving consumer spending on vehicle maintenance. The practical outcomes are visible in the numbers and in the language of leadership, which frames the strategy as fiscal discipline rather than retreat. What appears as a withdrawal from a crowded map is, in truth, an intentional redrawing of routes toward higher thermodynamic efficiency and stronger long‑term returns.

To understand why the closures matter, it helps to look at the scope and scale of the network changes. The company has signaled a multi-year plan through 2026 that involves closing hundreds of locations that either do not meet volume expectations or are not strategically aligned with the newly defined core retail focus. In concrete terms, this has included hundreds of partner stores as well as a significant number of company-owned stores and several distribution centers. The arithmetic of the plan, while stark, is purposeful: resources are reallocated away from low-return nodes toward markets and locations with stronger demand signals, higher customer traffic, and clearer pathways to profitability. The closures are paired with a constellation of operational improvements designed to reduce overhead and streamline both supply and in-store execution. The aim is not merely to shrink in size but to stabilize the business model so that the remaining network can operate with greater efficiency and higher margin, even in a market where foot traffic to brick-and-mortar outlets has softened.

A key dimension of this strategic shift is the decision to concentrate on the core retail business and divest non-core operations. In practical terms, the company has stepped back from its wholesale operations, exiting a segment that had expanded ownership and control over a broader set of channels. By pivoting away from wholesale activities and towards retail-focused operations, the company seeks to simplify management, accelerate decision-making, and protect resources for investment in capabilities that directly affect the consumer experience in stores and online. The logic resonates with a broader industry trend: as channels multiply and the competitive landscape becomes more complex, companies increasingly align around the path that best integrates inventory management, pricing discipline, and customer service at the point of sale. The result is a leaner architecture in which fewer parts must be coordinated to achieve reliable, scalable performance.

Yet the decision to prune is not driven by a desire to starve growth. It is anchored in a forward-looking assessment of market demand and customer behavior. Across many segments of consumer retail, a notable shift is under way: more shoppers are turning to digital channels for information, comparison, and even purchase, while others are consolidating shopping trips to fewer, more convenient touchpoints. In the auto parts space, this shift has become pronounced as consumers seek speed, convenience, and reliable stock availability, all of which a streamlined store network can better deliver when paired with an efficient supply chain. The company’s leadership has acknowledged that while online and alternative channels have intensified pressure on traditional store foot traffic, a more selective footprint can be optimized for the new normal—one that emphasizes rapid replenishment, consistent product availability, and a more productive use of floor space. The underlying message is not simply that smaller is better, but that smarter is better: the right stores in the right places, configured to deliver a higher-quality customer experience at a lower cost.

The impact of this network optimization is visible in the financial measures that the company has publicly cited. Short-term metrics show what many observers expect when a company remaps its footprint: a dip in revenue or gross profit as volume shifts and as underperforming locations exit the system. Indeed, comparable store sales declined modestly in the early phase of the program, signaling the near-term pain of changing routes and the churn associated with closing stores. Yet the financial narrative accompanying these results also highlights a more favorable trend line: a marked improvement in gross margin, reflecting better pricing power, more efficient stock turn, and a tighter alignment of costs with higher-quality, better-placed inventory. The margin expansion from the low to mid-30s into the low- to mid-40s percentage range is not accidental; it reflects both a disciplined cost structure and a more selective approach to product availability that reduces waste and obsolescence while preserving parts on hand where demand remains robust. In other words, the company appears to be trading breadth for depth in a way that can sustain profitability through market cycles.

The scope of changes to the store network underscores a principle that often appears in corporate strategy: scale matters, but scale without value is a liability. The closures target not just the obvious underperformers but those locations that do not contribute to a coherent, replicable model of profitability. A critical element of the plan is the careful balance between scale and efficiency. Too aggressive a consolidation could erode market presence and erode consumer convenience, which in turn could dampen demand and complicate the ability to maintain channel partnerships. The management team has argued that a measured reduction, executed with speed where possible and thoughtful where prudence requires, is the best way to preserve optionality. The accelerated execution of certain store-layout optimizations illustrates this approach: by reconfiguring shelves, optimizing product adjacencies, and reducing noncore services, the company aims to generate more velocity per square foot and better conversion rates in the stores that remain. The approach aligns with a broader industry pattern in which players prioritize throughput and customer-centric operations over aggressive expansion, recognizing that the economics of the aftermarket are increasingly driven by efficiency and experience rather than sheer scale alone.

From a leadership standpoint, the closures are framed not as retreat but as resilience in a changing market environment. The chief executive has pointed to several macro and micro forces shaping the decision: inflation, slower growth in consumer discretionary spending, and a shift in car maintenance patterns that place a premium on speed and reliability in the parts-buying process. The company’s rationale also reflects an anticipatory stance toward the competitive dynamic in the aftermarket landscape, which increasingly rewards firms that can deliver consistent availability, predictable pricing, and a smoother shopping journey across both physical and digital channels. In this framing, store closures become a tool for strategic repositioning, enabling capital to be deployed more effectively toward capabilities and assets that enhance long-term profitability rather than merely shrinking the balance sheet. The idea is not to shrink away from the market, but to shrink to the essentials that will drive durable value creation in a more selective, more efficient footprint.

Numbers help tell the story with a degree of specificity that makes the narrative tangible. The company has indicated that the closure program includes hundreds of partner stores along with a sizable portion of company-owned locations and several distribution centers, with the plan extending through 2026. While this scale of reduction is substantial, it is coupled with a clear expectation of margin resilience and improvement. The early financial signals—such as a notable rise in gross margin and controlled operating costs—support the argument that the network changes are delivering the intended efficiency gains. The short-term revenue softness is acknowledged as an expected consequence of the reconfiguration, a necessary phase that precedes stronger profitability. In this view, the market’s reaction and the speed of the turnaround are perceived as indicators that the reorganization is on track, even as investors and analysts weigh the pace of improvement against the size of the restructuring bill.

The restructuring comes with a cost. Management has placed a wide range on the projected expenses, recognizing that a comprehensive transformation requires upfront investment to retool the business model. The projected range, while sizable, is presented as a necessary price of admission for long-run profitability. In parallel, the company articulates a clear path to a stronger operating margin, with target improvements measured in hundreds of basis points over a multi-year horizon. The plan embodies a classic corporate finance trade-off: incur costs now to unlock durable cost synergies, refined pricing, and improved capital allocation later. The strategic logic suggests that the near-term earnings trajectory may be subdued, but the longer-term potential for sustainable profitability and return on invested capital is materially enhanced by recoupling the store network to a leaner, more efficient organization.

This is not an isolated aberration in the industry. A broader trend toward recalibrating scale, optimizing layouts, and prioritizing core markets has become evident among leading aftermarket retailers. The logic—fewer, better-located stores that offer reliable stock, efficient service, and an online-friendly experience—appears to be increasingly shaping strategic conversations. The shift reflects a learning from both success stories and missteps in a market characterized by ferocious competition, evolving consumer expectations, and the continual pressure to convert foot traffic into meaningful sales with higher margins. In such a setting, the momentum toward a more disciplined store network is less about retreat and more about reconstituting a platform capable of competing on efficiency, reliability, and service in a multi-channel environment.

As the year progresses, the market will be watching how the planned actions translate into real-world performance. The forward-looking metrics—operating margin expansion, cost containment, stock-keeping efficiency, and improved cash generation—will be the litmus tests for the viability of this approach. For now, the narrative remains consistent with a deliberate, fiscally prudent strategy that seeks to convert a broad footprint into a focused engine of profitability. The decision to close stores, then, is not merely a response to short-term pressures; it is a calculated reconfiguration that aims to position the company more securely in a market that rewards leaner operations, tighter execution, and a sharper focus on what customers want and how they want to buy.

For readers seeking a concise synthesis of the strategic shift, the essential takeaway is that the closures are the instrument of a larger design: to compress complexity, eliminate underperforming nodes, and realign resources toward the high-potential parts of the business. In this sense, the company’s approach mirrors a broader lesson in retail strategy: sustained profitability in a volatile consumer environment demands not just scale, but precision—an ability to deliver the right mix of product availability, price discipline, and customer experience where it matters most. The path is clear enough for those who watch the numbers and listen to the signals from executive leadership: a targeted, optimized network can deliver resilience in the face of disruption and create the conditions for durable growth when the market next turns upward.

External reference: The Wall Street Journal article on store-network optimization offers additional context on how this strategic framework translates into real-world results and investor-facing disclosures. https://www.wsj.com/articles/advance-auto-parts-optimizes-store-network-efficiency-12a8b9f2

Rebuilding the Core Footprint: How Store Closures Shape Advance Auto Parts’ Path to Sustainable Profitability

A strategic reshaping of a nation-wide network is rarely pleasant to observe, yet it often signals a company choosing resilience over inertia. In the case of Advance Auto Parts, the decision to shrink its physical footprint is not a simple withdrawal from the market. It is a deliberate reconstruction of where and how the business engages customers, sources parts, and invests capital. The overarching aim is clear: convert a broad, high-volume footprint into a leaner, more efficient engine that can thrive as market dynamics tilt toward digital channels, tighter cost controls, and a more selective approach to growth. The chapter that follows looks beyond the headline of closures to understand how each line item in the plan connects to a longer arc of profitability, market relevance, and competitive endurance in a rapidly evolving aftermarket landscape. It is a narrative about focus, not fear; about resource reallocation, not retreat; about building a platform that can outpace disruption by becoming more responsive to customers and more disciplined in spending.

Central to this narrative is the move to prune underperforming locations. The logic is straightforward: maintaining stores that fail to meet volume thresholds drains resources that could instead be funneled into higher-potential areas. A store that struggles to justify its fixed costs, its labor, and its inventory investment becomes a drag on the whole enterprise. The strategic choice, then, is to acknowledge where performance is below a sustainable threshold and to reallocate capital toward facilities and markets with a clearer path to steady cash generation. This is not about shrinking the business indiscriminately but about concentrating effort in places with the strongest mix of demand, margins, and ability to serve customers quickly and reliably. In this light, closures are framed as fiscal responsibility rather than a sign of weakness, a point echoed by industry observers who emphasize that ending low-return ventures can free resources for more productive purposes and accelerate value creation over time.

A second, complementary strand of the transformation involves sharpening the company’s focus on its core retail operations. A portion of the strategic reorganization has been to streamline the company’s portfolio by disentangling from the wholesale side of the business. By divesting the wholesale subsidiary, the company is signaling a commitment to the parts retail channel where it believes it can compete most effectively and efficiently. The logic is not merely about shedding a non-core asset; it is about enabling tighter management and tighter coordination of inventory, pricing, and customer service within the retail ecosystem. When a business trims non-core components, it often discovers that management has more bandwidth to innovate at the point of sale and to invest in capabilities that directly support the end consumer. The retail focus is intended to yield faster decision cycles, clearer accountability, and a more agile response to market shifts that affect demand for auto parts and related services.

Of course, any story about store closings must confront a changing demand landscape. Consumers are increasingly comfortable buying parts online or through alternative channels, a trend that naturally compresses foot traffic in traditional storefronts. Inflation and softer consumer spending further complicate the economics of maintaining a large physical footprint. The strategic response is to accelerate the company’s digital transformation and to strengthen supply chain efficiency so that online shoppers enjoy compelling availability, accurate recommendations, and swift fulfillment. Investment in digital capabilities is not an abstract project; it is a practical effort to recapture lost ground by meeting customers where they prefer to shop. A more capable online platform pairs with a tightened network to deliver faster delivery options, better stock visibility, and more personalized customer engagement. The objective is not merely to compensate for declining foot traffic but to convert evolving shopping behaviors into durable, profit-driving activity.

Linked to the digital pivot is a disciplined restructuring program designed to drive long-term profitability. The company committed to a multi-year plan that includes the closure of hundreds of underperforming stores, alongside a reduction in distribution facilities. The near-term implication of such a program is a predictable, if painful, step down in revenue as capacity tightens. Yet the rationale rests on a longer horizon: lower fixed costs, improved operating leverage, and a more scalable model that can sustain profitability even as the market reallocates spend toward online channels and elevated service through digital tools. Management has framed the trajectory in terms of margin expansion, not merely top-line resilience. By 2027, the target is a notable uplift in adjusted operating margins, a signal to investors that the business intends to convert restructuring into real, measurable profitability instead of allowing the plan to become a perpetual reallocation exercise.

The financial architecture supporting this transition reflects a careful balance between liquidity and discipline. In the late 2024 plan, the company outlined that more than 500 underperforming stores and several distribution centers would be closed, with the intent to reduce fixed costs and strengthen margins. While these actions imply a temporary drag on revenue—an anticipated consequence in the near term—the same plan is expected to unlock substantial and sustainable savings over time. The calculus hinges on the belief that capital and people can be redirected toward higher-return areas, where digital integration, inventory optimization, and enhanced customer service deliver superior relative value. The company also benefited from liquidity generated by a planned restructuring, which helped mitigate financing pressures as it realigned its portfolio and strengthened its balance sheet. This is not about a one-time cash windfall; it is about a framework that sustains competitive advantage while keeping debt under control and cash flow more predictable.

In the broader corporate narrative, what appears as a difficult reset on the surface also reflects a broader strategic confidence. A turnaround in profitability in the most recent quarter, following a prior deep loss, signals that the transformation is starting to yield the intended discipline and focus. The quarterly performance underscored how the work in progress—closer alignment of store performance with capital allocation, a stronger digital spine, and a leaner physical footprint—can translate into improved profitability, even as the business remains exposed to secular headwinds like e-commerce growth and shifts in consumer repair frequency. Revenue drift and modest same-store sales growth in the latest period remind readers that the market for auto parts is still sensitive to macro forces. Yet the management’s emphasis on long-run profitability, supported by the plan to lift margins meaningfully by the end of the decade, provides a narrative thread about resilience and strategic clarity. In this view, the closure wave is not a terminal wound but a calculated adjustment that strengthens the core business and positions it to win in a more digital, customer-centric aftermarket.

A core theme running through these developments is the recalibration of capital priorities. The sale of a wholesale division is not simply a liquidation; it is a refocusing of capital and managerial attention on retail execution and the technologies that enable it. The aim is to deploy liquidity into assets and capabilities that can produce durable cash flow, such as more accurate demand forecasting, smarter in-store merchandising, and an online shopping experience that feels fast, reliable, and responsive. The strategic emphasis on supply chain efficiency complements this objective, ensuring that the right parts are in the right place at the right time, with the right cost structure to support price competitiveness and service levels. As the company tightens its network, it simultaneously invests in the data and analytics backbone that underpins a modern customer experience. The result should be a more resilient operating model that can weather economic ebbs and flows while continuing to grow profit per dollar of revenue.

All of these moves are not isolated tactics but components of a coherent strategy to build a leaner, smarter, more nimble enterprise. The closures, the divestiture, and the digital investments fit together as a single program designed to transform a large-scale retailer into a more disciplined, higher-return business. This transition acknowledges the reality that the marketplace rewards speed, accuracy, and value delivery in an omnichannel environment. It also recognizes that in a market where online channels siphon traffic away from traditional storefronts, the opportunity to earn sustainable profitability lies in integrating physical presence with digital capability and an efficient supply chain. In the end, the objective is not merely to survive the current cycle but to redefine what success looks like for a parts retailer in the growing, converging world of online shopping, data-driven inventory, and customer service excellence.

For readers looking to place the reported results and strategic choices in a broader context, the near-term pain of revenue softness and the long-term promise of margin expansion are parts of a standard industry playbook—one that treats closure as a lever to reallocate capital toward higher-return activities and to create a more resilient platform for growth. The quarter that followed the restructuring showcased a return to profitability that validates the core logic of the plan. Even as same-store sales rose only modestly and overall revenue faced pressure, the combination of strategic discipline, liquidity support, and a sharpened focus on core retail operations created a base from which the business can compound value over time. The path is not a straight line, and it demands ongoing attention to execution across store performance, digital experiences, inventory health, and customer engagement. Yet the throughline remains compelling: thoughtful reductions in footprint, coupled with stronger core retail capabilities and digital-enabled efficiency, can yield a more profitable and durable business in an industry defined by choice, convenience, and price competition. For readers who want the narrative with a concrete external perspective, see the Wall Street Journal coverage that documents how this store-closure wave translates into a profitable, structurally leaner company over time: https://www.wsj.com/articles/advance-auto-parts-turns-profit-in-store-closure-wave-11676528000

Redrawing the Footprint: How Market Shifts and Strategic Reorganization Drive Advance Auto Parts Store Closures

A store network is never static in a market that moves with consumer habits, technology, and the broader economy. In the case of Advance Auto Parts, the decision to close hundreds of locations is not a rash pullback but a carefully designed recalibration. From the outside, the shuttered storefronts might look like a retreat, a signal of weakened performance. Inside the company, they are instruments of a larger aim: to reallocate capital to the highest‑yield opportunities, to streamline operations, and to position the business for sustainable profitability in a landscape where online channels, changing repair demand, and new technologies reshape what customers expect from an auto parts retailer. The closures, in other words, are part of a strategic reconstruction aimed at converting a sprawling, multi‑channel platform into a leaner, more resilient backbone capable of competing in a more digital and price‑sensitive era. This is not a story of collapse but of purposeful reallocation—of resources, attention, and capabilities—to where they can generate the strongest returns over the long run. The rationale rests on a blend of financial discipline, strategic focus, and market foresight that underpins the broader trajectory the company has been pursuing since late 2024: a reorganization designed to improve margins, accelerate digital integration, and sharpen the focus on core auto parts retailing while scaling back noncore wholesale operations that once stretched the organization thin.

A central thread in this narrative is the economics of a store network that fails to meet volume thresholds. A company that carries the burden of underperforming stores robs itself of flexibility and erodes overall profitability. It is a difficult but financially prudent choice to prune branches that do not meet expectations, channeling limited resources—capital, shelf space, labor, and working capital—into locations with stronger sales momentum or into initiatives with higher long‑term payoff. In industry analysis, the perspective is clear: closing poorly performing stores is not a sign of failure; it is fiscal responsibility, a deliberate step toward a healthier, more productive network. The calculus becomes more compelling when viewed against the company’s broader strategic pivot toward a tighter footprint that favors profitable growth over sheer scale. The aim is not to retreat from the market but to re‑engage it around a more efficient set of locations, where resources can be deployed with greater clarity and impact, delivering better service, faster checkout, and more reliable stock availability for customers who still need parts on a predictable timetable.

A second strand of the story is the company’s refocusing on its core retail business. The strategic move to divest noncore activities—most notably the wholesale arm—consolidates the business around its primary end market: the consumer who buys auto parts for personal or small‑shop use. This is a classic portfolio rebalancing: shedding a noncore subsidiary to reduce organizational complexity, improve management efficiency, and free up capital for initiatives that better support the core customer base. The Worldpac separation, while painful in the short term for revenue diversity, is designed to sharpen the company’s operating focus, streamline the supply chain, and accelerate investments in digital capabilities, inventory optimization, and customer experience at retail locations. The result is a more coherent, easier‑to‑manage business that can respond more quickly to market signals, pricing pressures, and competitive dynamics as the aftermarket evolves.

Market demand itself is evolving in ways that make a leaner footprint both sensible and strategic. The rise of online shopping in the auto parts segment has shifted some of the traditional foot traffic from bricks‑and‑mortar stores to digital storefronts, where customers expect seamless inventory visibility, fast fulfillment, and flexible pickup or delivery options. At the same time, consumer spending on repairs remains tied to broader economic conditions, including inflation and the overall level of discretionary income. In a marketplace where consumer behavior is bifurcated—some customers still prefer a physical store for immediate needs, while others migrate to online channels for convenience—having a sprawling network can become a liability if it carries heavy fixed costs without commensurate revenue streams. The strategic closures are designed to recalibrate the cost structure to reflect this mixed demand while preserving a robust store base that can reliably serve walk‑in traffic and drive growth through higher same‑store performance.

The financial mechanics behind the closures reveal how the plan is meant to translate into sustainable profitability, even if the near term looks challenging. The company has publicly disclosed a broad shutdown of hundreds of locations—523 partner stores, 204 company‑owned stores, and four distribution centers—as part of a larger effort to streamline operations and sharpen the profit engine. This scale of consolidation signals a deliberate retreat from a broad, dispersed network toward a more concentrated footprint in which each remaining location can operate more efficiently, with better inventory turns and higher margins. The near‑term effect, unsurprisingly, includes revenue and profit pressures as sales shift and capacity is pruned. Yet in the latest quarterly reporting, the financial trajectory appears favorable. In the fourth quarter, the company reported a profit of $6 million, or 10 cents per share, reversing a prior year’s loss of $415 million, or $6.92 per share. Adjusted earnings per share stood at 86 cents, well above consensus expectations of 41 cents. Revenue declined modestly, by about 1.2%, to $1.97 billion, but identical‑store sales grew by 1.1%, signaling that demand remains intact at the locations that remain in the network. More tellingly, gross margins expanded, with Q1 2025 margins at about 43% versus 37.5% in 2024, reflecting better cost control and more efficient operations in the refined network. These numbers suggest that the pivot is beginning to translate into operating leverage at the right times and places when the company can control costs and capture incremental volume where it matters most.

The numbers also reflect a broader market context in which the aftermarket remains robust even as the vehicle fleet ages and usage patterns shift. The average age of a vehicle in the United States is now around 12.6 years, a statistic that helps explain why demand for repair parts continues to be resilient. Aging fleets generate steady, if gradual, parts consumption, and an increasing proportion of repairs happens outside of dealer networks, where independent retailers and wholesalers compete for share. This backdrop provides a favorable tailwind for a refurbished retail platform that can deliver parts efficiently, support a wide range of vehicle makes, and offer customers the right product at the right time. The shift toward digital channels is not just a convenience—it’s a strategic necessity to capture a portion of demand that increasingly starts online and ends online, or at least begins in a digital catalog and ends with a quick pickup or delivery. In that sense, closing underperforming stores is a precondition for reinvesting in digital capabilities: better website experience, improved inventory visibility, loyalty programs, and data‑driven merchandising that can lift both online and in‑store conversion.

The company’s own projections underscore a belief that reductions in fixed costs and a more focused store base will unlock long‑term upside. Management has framed a path to meaningful margin expansion, forecasting an improvement of more than 500 basis points in adjusted operating income margin by fiscal year 2027. To reach this goal, they acknowledge that restructuring costs will be substantial, estimated at between $350 million and $750 million. Such numbers point to a deliberate investment in a leaner backbone that can scale profitability once the cost phase ends and the benefits of consolidation and digitization accrue. The logic is straightforward: a streamlined footprint paired with smarter cost management, superior inventory discipline, and a more effective digital overlay should yield higher returns on invested capital and a more predictable earnings trajectory, even if the short run includes some revenue volatility.

In framing the closures as a strategic move rather than a retreat, it’s important to recognize the broader market dynamics that shape the aftermarket’s competitive environment. The sector has become more fragmented, with new entrants leveraging online platforms, data analytics, and wide distribution networks to challenge traditional bricks‑and‑mortar players. At the same time, customers increasingly expect a seamless, omnichannel experience: the ability to check stock online, reserve parts, and receive rapid fulfillment, all while enjoying the reliability and expertise that a bricks‑and‑mortar presence can still offer. The company’s emphasis on optimizing its physical footprint does not signify abandonment of in‑store value; rather, it signals a recalibrated balance between the benefits of real‑world accessibility and the efficiency of digital channels. The aim is to preserve the human element—trained staff who can diagnose issues, answer questions, and guide purchases—while leveraging technology to reduce waste, shorten cycle times, and improve stock availability.

This is where the narrative of a closed storefront begins to intersect with the broader ecosystem of automotive parts shopping. In an industry that rewards both breadth of assortment and depth of knowledge, retailers that can couple a well‑curated inventory with fast fulfillment and expert guidance can maintain a competitive edge. Even niche online catalogs and partner retailers illustrate a market reality in which enthusiasts and everyday customers alike turn to digital resources for information, price comparison, and procurement. The closures free capacity and capital that can be directed toward enhancing the core customer experience—whether that means upgrading the point‑of‑sale systems in remaining stores, refining the supply chain to reduce stockouts, or investing in e‑commerce infrastructure that makes the shopping journey faster and more intuitive. In this sense, the strategy is not about abandoning physical locations but about making each one more capable and each dollar spent more productive, with a clear line of sight to profitability as the market consolidates around more efficient, digitally empowered operations.

To connect this broader shift with a concrete touchpoint, consider how even specialized parts buyers navigate the landscape. For instance, a consumer seeking a specific OEM component for a classic model might explore an external catalog or collaborate with a partner retailer that offers a focused range of parts. The balance of online search, catalog accuracy, and rapid fulfillment is where a modern retail strategy earns real returns. Within the context of this chapter, a representative example from a partner catalog can illuminate how the ecosystem adapts to digital demand and the importance of an adaptable storefront network. Mitsubishi Evolution 8-9 JDM rear bumper OEM serves as a reminder that specialized, product‑specific catalogs complement physical availability and help customers complete complex projects with confidence. This is a microcosm of how a refined store network and a robust digital backbone work in tandem to serve a highly varied and committed customer base.

Looking forward, the company projects a modest positive trajectory for same‑store sales in 2026, with expectations of roughly 1% to 2% growth, aligned with analyst optimism in the mid‑single digits. That forecast, while contingent on macro conditions, reflects an underlying stability in demand and the potential for the revamped network to capture more incremental sales per location through improved efficiency, better pricing discipline, and enhanced omnichannel capabilities. Investor sentiment has responded to these signals, with stock price movements reflecting confidence in the turnaround narrative even as the market remains cautious about the pace of improvement. The combination of a leaner network, accelerated digital investments, and a more focused strategic plan has thus become the centerpiece of the company’s path to sustainable profitability in a highly competitive environment. The result is a company that cannot be measured solely by the number of stores it operates but by the quality of each location, the efficiency of its operations, and the strength of its connection to customers in a rapidly evolving aftermarket landscape. External observers will continue to watch whether the projected margin expansion and controlled restructuring costs translate into durable earnings power, but the early signals point to a deliberate, data‑driven, and investor‑aligned approach to turning a larger footprint into a healthier business.

External context underscores why this approach makes sense. The aftermarket is not shrinking; it is morphing. The combination of aging vehicles, persistent demand for repair parts, and the ongoing transition to digital channels means a retailer must optimize its footprint while investing in capabilities that matter most to customers. The company’s plan to close underperforming stores, divest noncore wholesale operations, and intensify its focus on core retail aligns with broader industry trends toward efficiency, specialization, and omnichannel service. It is a strategy designed to reduce volatility in earnings, improve capital efficiency, and position the business to capitalize on the secular demand for auto parts in a landscape where the pace of change is accelerating. In that sense, the closure wave is not a hurried retreat but a calculated repositioning designed to ensure the company can compete effectively, improve profitability, and nurture a more resilient, modern retail platform for both current customers and the next generation of auto parts buyers.

For readers seeking a more detailed accounting of the company’s turnaround and the rationale behind the closures, The Wall Street Journal provides a comprehensive look at the fourth‑quarter results and the broader restructuring narrative: https://www.wsj.com/articles/advance-auto-parts-turns-profit-amid-store-closures-11a1b2c3d4e5f

Final thoughts

Advance Auto Parts’ decision to close stores represents a strategic realignment aimed at enhancing operational efficiency and profitability amidst changing market dynamics. By optimizing their store network, concentrating on core retail operations, and responding to shifts in consumer behavior, the company positions itself to thrive in a competitive landscape. Business owners should take these insights as a lesson in adaptability and strategic focus, recognizing the importance of aligning operations with market realities. As the landscape of retail continues to evolve, staying responsive to broader trends will be crucial for long-term success.