The recent announcement of store closures by Advance Auto Parts has raised questions among business owners regarding the company’s direction and future prospects. Many may wonder if these closures are a precursor to a wider trend or if they signify something more strategic. This article delves into the reasons behind these closures, the financial implications they pose, and the broader market trends that are shaping the future of Advance Auto Parts. Each chapter aims to offer a comprehensive overview to better understand the motivations and expected outcomes of this pivotal decision.

Why Advance Auto Parts Is Closing Stores: A Strategic Shift, Not a Full Exit

Why Advance Auto Parts Is Closing Stores: A Strategic Shift, Not a Full Exit

Advance Auto Parts’ decision to close a large number of stores has stirred questions about the company’s future. The short answer is that this is a targeted restructuring aimed at long-term health, not a wholesale shutdown. The company is pruning locations that underperform, overlap with other outlets, or sit in persistently low-traffic zones. This is a calculated pivot meant to sharpen competitive positioning and reallocate resources where returns are strongest.

At the core of the strategy is a simple financial reality. Operating many small, low-volume stores is costly. Lease renewals, property taxes, wages, utilities, and inventory carrying costs add up. When a location serves too few customers, the per-transaction cost can eclipse any margin advantage. Closing stores that consistently miss volume thresholds reduces overhead and lets management concentrate investment in higher-return channels and markets. That discipline helps protect margins and frees capital for modernization efforts.

Market dynamics make the choice more urgent. Consumer behavior has been steadily shifting toward online purchasing. Customers now value convenience, fast shipping, and broad selection. Large online retailers and dedicated e-commerce competitors can often undercut prices or deliver products to customers quickly. In response, Advance Auto Parts is accelerating its focus on digital channels, fulfillment networks, and inventory strategies that support both online and in-store demand. The goal is not merely to cut costs but to reposition the company for a hybrid retail environment.

Financial performance explains part of the urgency. The firm reported a modest net sales decline in a recent quarter. Several operational disruptions, including a major system outage at a third-party cybersecurity provider and severe weather in certain regions, contributed to that weakness. Still, the company posted a resilient gross profit figure, reflecting effective inventory management in prior quarters. That gross profit provided a cushion and highlighted that profitability levers still work when inventory and assortment are optimized.

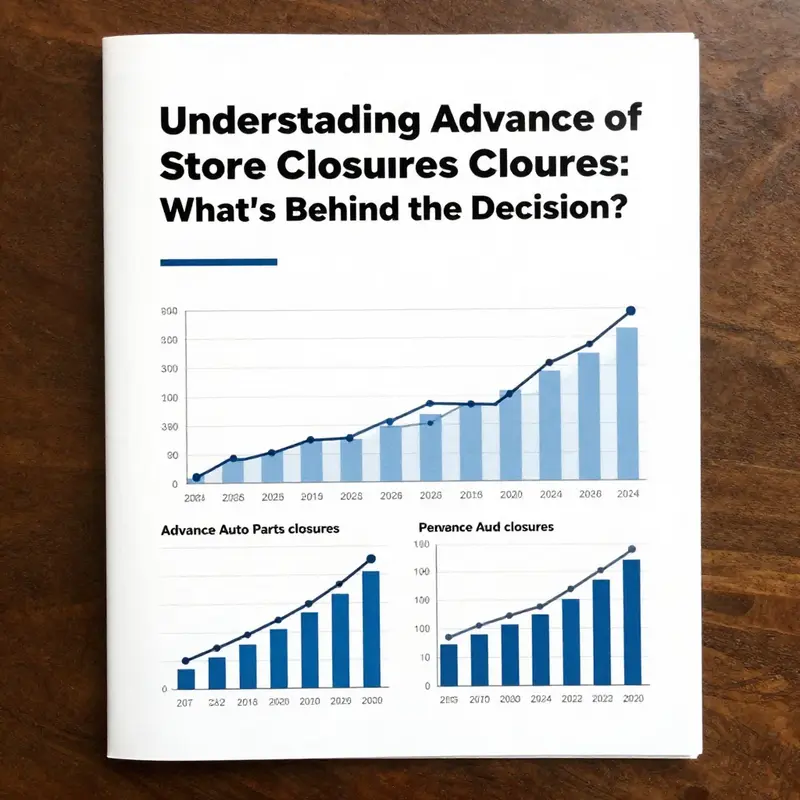

The scale of the announced closures is substantial. The company plans to shutter more than five hundred underperforming stores and to retire a handful of distribution centers. While the headline number sounds large, the arithmetic clarifies the rationale. Management expects the closures to reduce annual net sales by roughly eight hundred million dollars. That decline in topline revenue is balanced against meaningful cost reductions and margin improvement. In other words, the company is accepting a smaller but healthier business footprint.

Management’s financial targets make the intent clear. The strategic plan aims for a materially higher adjusted operating margin in the medium term. The company has set a target to reach an adjusted operating margin of seven percent by 2027. Nearer-term, the restructuring should lift adjusted margins to two to three percent by the end of the next fiscal year. Those targets rest on several pillars: better store productivity, more efficient supply chains, and greater leverage from digital sales. The math is straightforward: fewer unproductive stores reduce fixed costs, while improved fulfillment and assortment choices let gross margin expand.

Restructuring often triggers concern about customer access and local jobs. Management frames the closures as surgical. They will focus on stores that chronically miss volume thresholds, are in low-traffic neighborhoods, or are redundant because of nearby locations. In many communities, customers will still have nearby retail options, either other physical locations or enhanced online ordering with rapid delivery or convenient pickup. The firm also plans to open approximately thirty new stores in higher-potential markets. Those openings are part of a rebalancing, not a net withdrawal from retailing.

Operational improvements accompany the closures. The company is investing in better inventory planning and data-driven workforce practices. This includes dynamic scheduling to match staffing with customer traffic, more precise replenishment algorithms, and stronger collaboration with supplier partners to lower fulfillment costs. The aim is to deliver the right product to the right place at the right time, whether that place is a store shelf or a customer’s front porch. These changes are intended to preserve customer service levels while reducing the capital and operating costs tied to an oversized physical footprint.

The strategy also includes supply chain rationalization. Retiring certain distribution centers is painful but often necessary when parcel and freight economics change. Consolidating logistics can reduce duplicated routes and improve density, which cuts transportation costs and delivery lead times. Those benefits support both the online business and the remaining retail network. The company expects savings from these logistics moves to contribute materially to improved margins over time.

Another lens on this decision is the concept of store productivity. A well-performing store pays for fixed costs and then contributes to corporate profitability. A poorly performing one drains resources and distracts management. Closing stores that consistently underperform improves average productivity across the chain. Higher productivity makes each remaining store more valuable and more capable of supporting investments in customer experience. That virtuous cycle helps explain why the company is willing to accept a near-term sales reduction in exchange for better long-term profitability.

Communicating the reasoning to stakeholders matters. Investors want to see credible pathways to improved profitability and sustainable returns. Employees seek clarity about how the changes will affect their roles. Local communities deserve to know how closures will affect access to parts and services. The company has laid out projections that show a transition period, followed by gradual margin improvement and a path back to profitability. Management expects adjusted earnings per share to recover and grow in the years after the restructuring, and it has provided revenue guidance that reflects both the closures and new investments.

Execution risk is real. Closing stores carries costs: lease termination fees, severance, inventory write-downs, and the administrative burden of winding down operations. Those near-term costs can depress earnings in the short term. That is why the timing and sequencing of closures matter. Doing too many at once can disrupt supply chains and reduce customer confidence. Doing too few can delay the financial benefits. The company has signaled a phased approach, combining closures with targeted openings and investments in fulfillment. Phasing helps manage cash flow and preserves service continuity.

Competitive response will shape outcomes. Rivals can react by cutting prices, expanding digital capabilities, or adjusting their own store footprints. The company must keep the customer at the center of its choices. Enhanced online searchability, faster delivery options, and improved in-store pickup experience help defend market share. Equally important is ensuring that remaining stores remain convenient and well-stocked. Customers who try an online experience and find it lacking are less likely to return.

Beyond pure economics, the decision reflects a broader industry trend. Many retailers are rethinking how physical space complements digital channels. The most successful players view stores as nodes in a broader omnichannel network. Stores can drive sales directly, serve as pickup and return hubs, and act as marketing touchpoints. The challenge is to align the physical footprint with the realities of modern shopping habits. For this company, the calculus favors fewer, better-located, and better-equipped stores rather than a dense network of marginal locations.

For customers wondering what this means practically, the message is layered. Local availability of parts may change in some markets, but alternative fulfillment options will expand. The company plans to lean into digital ordering, same-day delivery in select areas, and expedited store pickup where stores remain open. Those options are intended to compensate for closures and maintain accessibility for customers who rely on timely parts and advice.

Finally, the strategic choice is a statement about priorities. Rather than trying to maintain market share through sheer scale of locations, the company is prioritizing margin, cash flow, and long-term viability. That shift recognizes that growth for its own sake can be hazardous when consumer preferences and cost structures change. By focusing on profitability and operational soundness, management aims to create a business that can invest in technology, strengthen supplier relationships, and return to sustainable growth.

The decision to close a significant number of stores is not the end of the company’s retail presence. It is a redefinition of what that presence should look like. For shareholders, the move promises improved margins and a clearer path back to earnings. For customers, it promises better inventory, faster fulfillment, and more reliable service in the markets that matter most. For employees and local communities, it is a transition that will require careful management and transparent communication.

This chapter has described the strategic logic behind the closures. The company views the action as disciplined portfolio management. Closing underperforming stores reduces drag, frees capital for investments, and supports a modern retail model that blends physical and digital strengths. The hope is that a leaner footprint will produce a healthier company, one that can compete on service and convenience while delivering consistent returns. For full context on the company’s financial outlook and strategic direction, see the detailed industry coverage and official reporting linked below.

Source: https://www.wsj.com/articles/advance-auto-parts-store-closures-turns-profitable-2026

Selective Contraction, Lasting Growth: Reading the Financial Logic Behind Advance Auto Parts’ Store Closures

In markets where the pace of change accelerates, headlines tend to latch onto the most dramatic outcomes. When a retailer announces the closure of hundreds of stores, the instinct is to interpret it as a retreat. Yet the broader arc often reveals a more deliberate strategy: a selective contraction designed to reallocate capital, sharpen the operating engine, and invest in growth channels that better align with evolving shopping habits. This chapter follows that thread for Advance Auto Parts, a company that has been both the subject of intense public scrutiny and a case study in how a traditional brick-and-m mortar model can recalibrate without pulling away from customers who increasingly blend online and in-store experiences. The question in the public imagination—Are all Advance Auto Parts closing?—misreads the logic at work. The company’s action, though large in scale, reflects a targeted pruning of underperforming footprints in order to preserve and expand the parts business in a more digitally enabled, logistics-supported framework. In other words, this is not a blanket withdrawal; it is a strategic narrowing with a deliberate eye toward long-term profitability and resilience in an industry where the competitive differentiator is increasingly the speed, reliability, and reach of the supply chain as well as the ease of the shopping journey. The narrative, then, unfolds as a balance sheet story and a customer- access story, both driven by a shared objective: to convert density of stores into density of value for customers and shareholders alike.

The scale of the closures announced in late 2024 establishes the frame for understanding the financial logic behind the move. The plan targeted hundreds of locations—specifically more than 500 company-operated stores and roughly 200 independent franchise stores. This was not a random culling; it was a data-driven recalibration of the firm’s physical footprint. The criteria were clear: underperforming stores, low-traffic sites, and overlaps with nearby locations that diluted the incremental benefit of maintaining multiple outlets in the same region. In a retail world where the path to sustained growth increasingly runs through online channels, streamlined logistics, and faster fulfillment, those stores that could be served more cost-effectively from a central hub or a nearby alternative would become candidates for closure. The objective was not to shrink the business recklessly but to reallocate capital toward assets with greater potential to lift returns—areas where investments would yield faster, steadier payoffs, such as e-commerce capabilities and distribution center networks that improve the speed and accuracy of orders for both DIY customers and professional service providers.

Two sets of forces shaped the decision: the top line’s vulnerability in a slowing consumer environment and the bottom line’s sensitivity to the fixed costs that accompany a large brick-and-mortar network. In the short term, the closures accrued restructuring costs and other transition-related expenses. The third quarter of 2024 carried a noted net loss of around $6 million, reflecting these transitional charges and the ongoing challenges of consumer spending weakness. External disruptions added to the complexity. A CrowdStrike system outage, which affected security and operations for a period, and a severe weather event—Hurricane Helene—introduced operational headwinds that temporarily shadowed the company’s performance. Even so, the closure program did not derail the broader transformation plan; if anything, these early headwinds underscored why a leaner footprint could be the enabler for healthier margins and more predictable cash flow in the years ahead. The company’s leadership argued that the short-term softness could be absorbed because the long-term benefits would accrue from lower fixed costs and stronger capital allocation.

One of the most pivotal outcomes of the closure initiative was the immediate and meaningful improvement in operating efficiency that could free resources for more productive uses. Management estimated that the annualized savings from closing underperforming stores and four distribution centers would amount to roughly $70 million. The savings would stem primarily from reductions in rent, labor, utilities, and other operating costs associated with maintaining a large physical network that did not consistently translate into proportional revenue. Simultaneously, the company secured liquidity through the divestiture of a major subsidiary, generating liquidity that could be redirected toward transformation efforts. Although the headline figure of a $15 billion liquidity infusion is substantial and eye-catching, the more important implication for the business is the improved balance sheet position that makes it easier to fund investments in the needed assets—both digital and logistical—that support a more efficient service model.

The financial arithmetic of the strategy extended into the medium term. By the 2025 earnings cycle, the company outlined expectations that the cost savings from the closures would contribute to an expansion of the adjusted operating margin. The trajectory was clear: the reductions in ongoing costs would lift profitability, enabling a more favorable margin profile even as the company pursued selective growth initiatives. The results supported that view. In the fourth quarter of 2025, the adjusted operating profit margin achieved 3.7%, a stunning improvement of 870 basis points year over year. The gain was not instantaneous, but it was material and consistent with the plan: a business that could convert a leaner footprint into healthier margins while continuing to serve its customers effectively. The margin improvement was not merely a reflection of lower costs; it also reflected better capital discipline and a more purposeful allocation of resources toward growth enablers, including the expansion of network assets that could support higher service levels at scale.

At the heart of the strategy lies a deliberate reshaping of the company’s store count in conjunction with a broader push into growth assets that could compound over time. Management signaled confidence that the future lay in a more connected network of physical stores aligned with a robust digital presence and an upgraded logistics framework. The plan called for the opening of 35 new stores in 2025, signaling continued commitment to footprint growth even as a portion of the broader network was pruned. Looking ahead, the plan envisioned 40 to 45 new stores in 2026, complemented by 10 to 15 new market centers. These market centers were presented as the backbone of supply chain efficiency, featuring a wide SKU assortment—estimated at 75,000 to 85,000 SKUs—and serving 60 to 90 surrounding stores. The idea was not to simply stock more items; it was to stock the right items, more efficiently, in locations that would shorten replenishment cycles and improve on-time availability for both DIY customers and professional fleets. It was a design fit for a retail environment in which proximity mattered less than rapid access to the items customers need when they need them.

These strategic investments reflected a broader shift in capital allocation. Rather than protecting a bloated footprint that relied heavily on real estate as a primary driver of sales, the company steered cash toward capabilities that could support a more agile, customer-centric operating model. In practical terms, that meant funding additional distribution centers and market centers, enhancing digital sales tools, and building the logistics muscle necessary to compete with both large bricks-and-m mortar chains and online-specific retailers. The transformation also touched the balance sheet in meaningful ways. The company projected that positive free cash flow would return in 2026, targeting around $100 million, a reversal from a negative $298 million in 2025 that was driven in part by cash outlays associated with the store-closure program. This cash flow rebound was not merely a financial metric; it signaled a return to a more sustainable capital allocation cycle that could support ongoing investments in growth while generating durability in periods of economic uncertainty.

To be sure, the closure program was not without its critics or its challenges. The immediate negative effects on the quarterly results, the need to navigate a changing consumer environment, and the logistical complexities of shuttering dozens of locations in a short period were real and tangible. Yet the company’s leadership framed these challenges as transitional hurdles on the path to a more resilient, higher-return business. The long-run forecast underscored this view. The company anticipated that 2025 would mark the beginning of a sustained improvement in profitability, driven by the dual forces of cost discipline and selective expansion. The revenue outlook for 2026 suggested a stable growth trajectory, with the company guiding revenue in a range around the high eighties to mid-nineties—tens of billions, depending on macro conditions and the pace of the expansion. This outlook reflected confidence that the company could grow through a combination of new store openings, the efficiency gains from market centers, and the incremental revenue that would come from enhanced online channels and a more integrated service model.

From a strategic perspective, the closures should be understood as part of a broader operational upgrade rather than a retreat from core customer segments. The company did not signal any plan to abandon its traditional strengths in rapid parts delivery, hold times, or the breadth of parts offerings necessary to serve professional customers who rely on timely repairs. Instead, it positioned itself to compete more effectively by aligning its physical footprint with anticipated demand, reducing the fixed costs associated with underused square footage, and accelerating investments that would improve the entire customer journey. This includes a more seamless integration between online and offline channels, a more responsive inventory system, and a more robust infrastructure to support same-day and next-day delivery options where feasible. The end result would be a more resilient framework that could withstand the volatility of the macro environment while offering customers a consistently reliable way to find and receive the parts and accessories they need.

In this sense, the chapter closes not with a simple verdict on store closures but with a recognition of the kind of value a retailer creates when it repositions its assets around customer behavior. The closures serve as a catalyst for a rebalanced capital plan, one that invests in the elements most likely to produce durable profitability: a trimmed but more efficient footprint, stronger cash generation, and a logistics network capable of supporting a nationwide reach with tight inventory control. The company’s guidance for 2026—an expected return to positive free cash flow and an ongoing expansion in stores and market centers—reads like a clear map: shrink what does not perform, double down on what does, and use the resulting liquidity to fund capabilities that will reduce friction for customers across the shopping journey. In this narrative, the question “Are all locations closing?” fades into the background. The more relevant question becomes: which locations are closing, and how will the newly focused, more productive network improve service levels, speed, and choice for customers who increasingly expect an omnichannel experience? The answer lies in the balance sheet and the operating model, converging to outline a business that accepts the hard reality of a changing retail world while leaning into opportunities that come from smarter, more disciplined growth.

For readers who want to anchor these observations in the official financial chronicles, the quarterly and annual reports provide the granular numbers that bring the narrative to life. The closures themselves are clearly tied to measured cost savings and to tangible improvements in margins and cash flow over time. They are paired with a disciplined approach to growth, including the acceptance that some markets will benefit more from a new distribution hub than from another storefront, and that the path to customer satisfaction increasingly travels through speed, accuracy, and convenience as much as it does through a broad catalog of parts. In short, the strategy is built on balancing risk with opportunity: pruning underperforming parts of the network to invest in the parts of the network that can scale with demand and deliver reliable service in a landscape where competition remains fierce and consumer preferences continue to evolve.

Looking ahead, the overarching message is one of cautious optimism grounded in tangible financial milestones. The company’s 2023 net loss and the subsequent 2024-2025 reforms were not indicators of terminal decline but rather of a transitional phase that, if executed well, could yield a stronger, more resilient business. The projected margins, the positive free cash flow in 2026, and the planned pipeline of new stores and market centers all point to a model that maintains a robust physical presence while simultaneously driving a more efficient, digitally enabled operation. The real test, as always, lies in execution: the ability to translate the savings from store closures into higher-margin growth activities, and the capacity to convert a leaner footprint into a broader, faster, more reliable shopping experience for both DIY enthusiasts and professional technicians. If the mid-to-late 2020s deliver on these promises, the closures will be remembered not as an abrupt retreat but as a pivotal step in a deliberate transformation—one that redefines what it means to operate a national parts network in an era of accelerating e-commerce, tighter margins, and rising customer expectations.

External resources provide further context for the numbers and the timing of these strategic moves. For a primary, management-directed articulation of the financial trajectory and the outcomes of the quarter, consult the official earnings call transcript, which details the cost savings, cash flow expectations, and growth plans that underpin the narrative described here: https://www.investors.advanceautoparts.com/financials/default.aspx

Strategic Contraction, Not Closure: How Advance Auto Parts Is Reshaping Its Network for a Shifting Auto aftermarket

The headline question lingers in the minds of many observers: are all Advance Auto Parts closing? The simple answer is no. The fuller story is more nuanced and reveals a company steering through a transitional period with precision rather than retreat. On the surface, the plan announced in late 2024 to shut hundreds of stores might read as a blanket retreat from the physical retail footprint. Yet beneath that headline lay a deliberate, data-informed recalibration of the company’s network. The aim is not to surrender territory but to reallocate capital and focus toward higher-return opportunities. In this sense, the strategy resembles a disciplined pruning of a forest rather than a wholesale eviction. The combination of performance signals, market dynamics, and a company-wide push to modernize the consumer experience has created a narrative of selective closures that preserve the core strength of the brand while sharpening its future growth engines.

To grasp the logic, it helps to anchor the discussion in the timing and the content of the 2024 announcement. Advance Auto Parts signaled that a portion of its store base would be closed, but the action was explicitly framed as a strategic adjustment designed to optimize the retail network. The closures targeted underperforming locations, those in low-traffic zones, or sites whose footprint overlapped significantly with nearby stores. The practical effect was a consolidation of the physical presence, freeing up resources for the areas where the company sees the most opportunity to win with customers. This is not a liquidation of assets; it is a reallocation—redirecting investment toward the areas that increasingly define the modern auto parts ecosystem: online capabilities, omnichannel fulfillment, and regional distribution where speed and assortment can be controlled more efficiently.

That context matters because it reframes what a “closing” means in the current retail environment. The auto parts market has long depended on a blend of local accessibility and broad product availability. In recent years, the balance has shifted as online shopping, mobile conveniences, and rapid-delivery expectations become standard. For a national retailer with thousands of SKUs, the challenge is to maintain broad assortments without the drag of underperforming doors. The strategic closures are a direct response to that challenge. They aim to reduce noise in the network, which helps the remaining stores and the company’s digital channels operate more cohesively. And the shifts are not happening in a vacuum. They occur alongside broader retail patterns where the most resilient players combine a leaner footprint with superior e-commerce and logistics capabilities.

The financial backdrop to this strategy adds color to the picture. The company faced a net loss in 2023, which underscored the urgency of a more rigorous approach to cost structure and cash flow. The 2026 guidance, however, carries a different tone. Management projected a return to profitability and modest growth in same-store sales, alongside an anticipated revenue range that, while still large in absolute terms, would reflect the company’s intent to discipline capital expenditure and optimize the mix of brick-and-mortar and digital assets. Put plainly, the company signaled that the path to sustainable profitability lies in a more targeted store strategy, not in an indiscriminate withdrawal from neighborhoods or regions. The closures are therefore an instrument of resilience rather than a political statement about the future of physical stores.

Beyond the mechanics of store closures, the broader narrative is connected to a set of market forces that are reshaping the auto aftermarket. One dominant trend is the rapid growth of the electric vehicle (EV) segment. As EV adoption accelerates, the product portfolio required to support these vehicles expands in meaningful ways. It is not merely about a few new components; it is about a different pace and cadence of parts life cycles, specialized batteries, charging-infrastructure accessories, and a growing set of high-tech maintenance needs. The marketplace that supports conventional internal-combustion engines is evolving, and a retailer’s success rests on aligning stocking strategies, supplier relationships, and service capabilities with that evolution. In practice, this means that a company like Advance Auto Parts must maintain the agility to shift inventory toward categories that gain prominence in the EV era, all while sustaining a reliable supply chain for legacy products that still power the millions of conventional vehicles on the road.

A second, closely linked trend is the rise of smart and connected vehicle technologies. Consumers are increasingly aware of and interested in features such as advanced driver-assistance systems, telematics, and integrated infotainment solutions. The aftermarket response to this trend requires more than simply stocking fuses and belts; it calls for a broader suite of repair and upgrade options, diagnostic capabilities, and knowledge resources that empower customers to maintain and optimize sophisticated systems. For a parts retailer, that translates into an inventory strategy that includes more high-tech components, compatible tools, and a workforce trained to discuss complex vehicle systems with customers who demand clarity and confidence in every purchase. The store experience, therefore, must blend product availability with expert guidance, enabling customers to complete more of their projects in one trip or through a seamless online-to-store hybrid workflow.

Competition is another decisive force shaping the evolution of the network. The automotive aftermarket is intensely competitive, with well-capitalized rivals expanding their digital footprints while pursuing aggressive pricing and broad assortments. The ascent of e-commerce and omnichannel experiences has raised the bar for what constitutes a compelling customer journey. In this environment, success hinges on a retailer’s ability to deliver speed, convenience, and personalized support at scale. That requires investments in digital infrastructure, mobile platforms, and data-driven decision-making. It also means rethinking store formats and locations to complement, rather than duplicate, what online channels offer. A compressed footprint in certain markets can be a strategic boon if it concentrates the most productive doors and tightens execution. In other words, the goal is not to shrink the overall opportunity but to reduce friction and create a more coherent, customer-centric ecosystem where online and offline work together in concert.

Sustainability and regulatory considerations further shape how a modern automotive retailer designs its network. Heightened environmental awareness, stricter rules around packaging and waste, and a growing emphasis on responsible sourcing push retailers to embed greener practices into their operations. Those considerations influence where to deploy capital, how to optimize logistics to reduce emissions, and how to communicate corporate responsibility to a customer base that increasingly factors sustainability into purchasing decisions. The strategic closure plan serves as a mechanism to reallocate resources toward initiatives with clearer environmental and social dividends, such as packaging optimization, smarter warehouse design, and investments in more energy-efficient fulfillment capabilities. In this sense, the closures are not just financial or logistical adjustments; they are part of a broader effort to align the company with evolving expectations from customers, regulators, and communities.

Macro conditions, including inflation and supply chain volatility, add a layer of risk and opportunity to any network optimization. A disciplined approach—diversifying suppliers, strengthening logistics, and improving stock turnover—helps insulate the business from volatility while enabling it to capitalize on favorable demand patterns when they emerge. The company’s forward-looking guidance for 2026 reflects this balance. It signals cautious optimism about top-line growth, modestly improving margins, and a path to sustainable profitability even as the external environment remains imperfect. In such a context, the decision to close specific stores emerges less as a crisis response and more as a strategic recalibration that preserves optionality for future expansion in the right places and at the right times.

For readers seeking a snapshot of the market milieu that informs these decisions, consider how capital markets and investor sentiment frame the narrative. Real-time data and analyses from financial platforms offer a lens on how market participants interpret the company’s strategic posture. While the underlying business remains rooted in tangible assets like inventory, distribution centers, and in-store staff, the value drivers increasingly hinge on digital channels, cross-channel fulfillment, and the ability to translate a strong brand into repeat customer engagement across channels. In this light, the store closures are a symptom of a broader modernization program rather than a terminal withdrawal from the physical retail landscape. The company’s road map appears designed to stabilize cash flow, improve operating efficiency, and position it to capture more share in a retail ecosystem that rewards speed, convenience, and expertise across both digital and brick-and-mortar fronts.

In discussing these shifts, it is also important to acknowledge what the closures imply for communities that rely on nearby stores for access to parts and repair guidance. Select closures may disrupt local access, particularly in rural or underserved markets. However, the logic of the plan is anchored in the belief that stronger online options, better-aligned store formats, and the proximity of distribution centers will ultimately enhance service levels for customers who can and will transact across multiple channels. The trend is not to abandon neighborhoods but to reimagine how a customer can reach a reliable assortment, obtain expert help when needed, and receive timely deliveries. In short, the approach is a strategic rebalancing of the network that acknowledges changing consumer behaviors while preserving the core functions customers expect from a national auto parts retailer.

A practical consequence of this approach is a renewed emphasis on the synergy between stores and digital channels. The most successful retailers today treat the physical and digital experiences as two sides of the same coin. Customers who begin a project online often want to finish in-store, where a team member can offer hands-on guidance, confirm compatibility, and supply tools for the job. Conversely, customers who visit a store may discover that online ordering or curbside pickup offers a faster or more convenient path to completion. The optimization plan is designed to improve the outcomes of both pathways. By closing doors that do not meaningfully contribute to this integrated experience, the company expects to free up capital that can be redirected toward improving online interfaces, expanding same-day fulfillment capabilities, and investing in regional distribution hubs that shorten delivery times from coast to coast.

The net effect of these strategic moves is a retail architecture that looks less like a sprawling network of roughly identical outlets and more like a curated ecosystem. There is a core of well-placed stores that function in harmony with centralized distribution capabilities and robust online platforms. The aim is to deliver an omnichannel experience that feels effortless to customers, whether they are shopping on a phone screen, a computer, or at a counter in a neighborhood store. This is exactly the kind of evolution that many in the industry view as essential in a time when consumer expectations are shaped by the convenience of e-commerce giants and the reliability of familiar local outlets. In that sense, the closure program should be interpreted not as a retreat but as a deliberate, forward-looking realignment designed to sustain and grow the business across a more complex, higher-velocity market.

The strategic narrative is reinforced by the practical realities of execution. Store-by-store decisions are underpinned by data: traffic analytics, sales per square foot, inventory turnover, and proximity to alternative access points like nearby stores or distribution centers. The aim is to maximize the probability of a profitable misalignment being corrected without sacrificing customer access. It also means that the company must continue investing in staff development and customer education. In an era where products and systems can be highly technical, customers increasingly value trusted guidance as part of the purchase experience. The stores that survive and thrive in this environment are those that can pair solid product availability with knowledge-driven service—an element that can differentiate a large retailer from more impersonal online-only platforms.

In this evolving landscape, it is natural to wonder how far the network will evolve and how quickly. The strategic plan’s tempo is a function of both market signals and the company’s own financial discipline. The goal is to reallocate resources to activities with higher velocity and higher expected return—most notably digital commerce, logistics infrastructure, and enhanced customer service capabilities. It is a plan that seeks to balance short-term profitability with long-term growth, acknowledging that some communities may experience shorter-term disruption while others stand to gain from faster delivery times, more comprehensive online catalogs, and improved in-store expertise. The narrative that emerges is one of selective, purposeful contraction aimed at preserving the core competitive strengths of the business while investing aggressively in the future momentum that will define the next decade in the auto aftermarket.

For readers who want to explore a concrete example of how the parts ecosystem continues to evolve in specialized ways, consider how the aftermarket accommodates high-value, performance-oriented components that require precise compatibility and expert installation. While the headline business remains broad and mass-market, there is a growing appetite for more advanced, high-tech offerings that support modern vehicle platforms. This dynamic reinforces the importance of balancing a wide, accessible catalog with targeted, high-skill categories. The closures, in this framing, become a tool to ensure that the company can fund and sustain advanced service capabilities without overbuilding underperforming locations. In other words, the strategic contraction serves the broader mission of delivering value across a diverse customer base by weaving together accessible inventory, expert assistance, and rapid, reliable delivery in a way that fewer, more efficient doors can support more effectively.

As investors and customers observe the unfolding trajectory, it is useful to keep the lens on real-time market signals. Stock performance and analyst sentiment provide a proxy for how well the market is interpreting the company’s operational and strategic moves. The broader takeaway is that the retail landscape—especially for automotive parts—has not settled into a single blueprint. The most successful players will be those that can combine disciplined network design with relentless execution on digital channels, a customer-centric service model, and a supply chain capable of absorbing volatility while maintaining price and availability discipline. In this context, the “closing” question dissolves into a more nuanced inquiry: which doors are being closed, and what doors are being opened in their place? The answers point toward a more cohesive, technologically integrated, and financially sustainable storefront network that remains committed to serving both DIY enthusiasts and professional technicians across a broad geography.

To close the loop on internal perspectives, it is helpful to reflect on how this strategy aligns with ongoing shifts in the broader retail environment. For decades, retailers that could scale physical footprints often enjoyed advantages of visibility and convenience. Today, the pendulum has swung toward a hybrid model in which the speed and convenience of online platforms increasingly dictate customer choice. The company’s plan to close a subset of stores is part of a larger transformation that recognizes this new equilibrium. It is not a capitulation to online-only rivals; it is a strategy to preserve a scalable, multichannel engine that can compete more effectively with both brick-and-m mortar peers and digital challengers. As markets continue to prize speed, reliability, and expert guidance, the company’s ultimate test will be to demonstrate that its optimized footprint can outperform a larger, less focused network. If the forecast for 2026 holds—moderate same-store growth, improving profitability, and a deliberate shift of capital toward high-potential initiatives—the closures will likely be viewed in hindsight as a prudent step in a longer journey toward resilience and sustained leadership in a fast-evolving aftermarket.

For readers curious to navigate beyond the high-level narrative, the following internal resource offers a look at a different corner of the automotive parts ecosystem, illustrating how specialized components fit into the broader parts landscape: https://mitsubishiautopartsshop.com/03-06-mitsubishi-evolution-8-9-jdm-rear-bumper-oem/. This example underscores how even within a global luxury-leaning subsegment, the industry relies on precise compatibility, robust supply chains, and a network that can deliver the right part to the right place at the right time. It also serves as a gentle reminder that the path to success in the aftermarket is not simply about broad availability; it is about curated depth, reliable logistics, and the ability to transform customer intents into outcomes. As the market tilts toward more complex vehicle architectures and faster delivery expectations, the capacity to integrate these elements into a coherent, customer-centric model becomes a core differentiator—and the reason why selective store closures, executed with care, can be a constructive, growth-oriented move rather than a sign of retreat.

Investors and industry watchers will continue to watch keenly how the company’s network optimization translates into real customer outcomes. If the plan succeeds, customers will experience fewer gaps between shopping channels, faster fulfillment, and more knowledgeable service—an alignment that reinforces trust and loyalty in a sector where reliability carries outsized weight. The chapter’s throughline remains clear: not all stores are closing, but the map is being redrawn in service of a more resilient, technologically enabled, and customer-focused auto parts ecosystem. The evolution mirrors a broader movement across the retail landscape, where the most durable players are those that blend disciplined cost management with relentless investment in the capabilities that customers want in the moment they want them.

External perspective can also illuminate the conditions shaping this evolution. For readers who want a real-time snapshot of the market’s assessment of the company’s trajectory, finance and data platforms provide up-to-date impressions of stock performance and analyst sentiment. A current reference point is Yahoo Finance, which tracks the company’s market position and forward-looking forecasts, offering a window into how the broader investment community interprets these operational changes and their implications for future profitability. See the stock quote and related analysis here: https://finance.yahoo.com/quote/AAP/.

In sum, the question of whether all Advance Auto Parts is closing dissolves into a more complex reality. The company is closing a subset of stores as part of a strategic upgrade to its retail network, a move designed to sharpen its competitive edge in a fast-changing environment. This is not a retreat from the physical footprint but a reimagining of it—one that leans into the strengths of omnichannel fulfillment, a more targeted store portfolio, and investments in the capabilities that matter most to today’s customers. The road ahead remains contingent on execution and market dynamics, but the blueprint is clear: a more focused, capable, and connected automotive parts retailer that can thrive amid the convergence of traditional retail, digital commerce, and high-tech vehicle maintenance needs.

Final thoughts

The store closures at Advance Auto Parts reflect a calculated response to evolving market conditions and financial pressures. Rather than a sign of retreat, these strategic adjustments aim to refocus resources towards growth opportunities in e-commerce and logistics. Business owners should recognize these changes as part of a broader industry trend, emphasizing the need for flexibility and adaptation in their own strategies. Understanding this landscape can empower you to navigate similar challenges and capitalize on emerging opportunities in your sector.