As major players in the automotive aftermarket space, companies like NAPA Auto Parts stir various sentiments and speculations related to their market viability. Recent employee feedback and trading patterns of its parent company raise questions about the operational stability of NAPA Auto Parts. Understanding the intricate factors of employee sentiment, customer feedback, and financial health will illuminate whether NAPA is positioned to endure as an indispensable retail outlet for automotive parts or if it is on the brink of decline. This exploration unfolds in a comprehensive analysis segmented into four pivotal chapters, each connecting dots to elucidate the overarching question: Is NAPA Auto Parts going out of business?

Independence in Focus: Why NAPA Auto Parts Isn’t Going Out of Business—and How a Major Restructuring Signals a Stronger Future

The question many readers bring to this chapter is urgent and simple: is NAPA Auto Parts going out of business? The public record as of February 2026 points decisively in the opposite direction. Rather than facing closure, NAPA stands at the threshold of a strategic inflection point. Its parent company, Genuine Parts Company (GPC), announced a sweeping plan to split its portfolio into two independent, publicly traded entities. The automotive parts and service business, anchored by the NAPA brand, would become its own company. This is not a retreat or a liquidation but a deliberate separation designed to sharpen focus, accelerate investment, and unlock greater value for shareholders. In short, the chapter is less about a company’s demise and more about a company reorienting itself to grow more aggressively in a changing marketplace.

That reorientation rests on several converging truths. First, the scale and resilience of the NAPA operation are undeniable. In 2025, the business unit posted robust sales that exceed the $150 billion mark. That level of revenue is not only a testament to a vast network but also to the enduring demand for a broad, dependable supply chain in the automotive aftermarket. Second, NAPA’s physical footprint remains extraordinary. The brand operates more than 5,800 stores, supported by a nationwide lattice of 60 distribution centers and an expansive network of about 15,000 NAPA AutoCare facilities. This isn’t a peripheral business with a handful of shops; it is a nationwide ecosystem that touches fleets, independent repair shops, and consumer customers across the United States. The nervous system of consumer and commercial automotive care runs through these points of presence, and the restructuring is designed to optimize how this system allocates capital, talent, and digital resources.

Behind the numbers, the strategic rationale of the split is straightforward in its logic. When a company holds multiple, distinct lines of business under one umbrella, it often faces competing priorities. One group’s growth agenda can be constrained by another’s cash needs, risk tolerance, or regulatory considerations. The decision to create two focused, independently traded entities aims to resolve those frictions. For investors, it can reveal clearer trajectories, allow more tailored governance, and provide the kind of strategic flexibility that is harder to achieve when multiple businesses share a single balance sheet. In this case, the automotive parts and service business gains the freedom to invest more aggressively in its specific market, accelerate digital modernization, and deploy capital in a way that aligns tightly with the pace of vehicle technology, consumer behavior, and the evolving needs of independent service providers.

Moreover, the restructuring satisfies a broader market dynamic. Investors have long argued that certain highly specialized, capital-intensive sectors perform better when kept separate from broader conglomerates with diversified risk profiles. In a split structure, each company can articulate a more precise strategy, optimize its cost structure, and pursue tailored partnerships that suit its unique customer segments. For NAPA, that means a sharper focus on the aftermarket, on the service ecosystem that surrounds parts distribution, and on the digital tools that customers increasingly expect as part of a seamless shopping and service experience. The shift isn’t merely about corporate form; it is about governance that accelerates execution, with the potential to unlock greater shareholder value as market conditions evolve.

This vision sits against a backdrop of steady customer activity and a large base of partners who rely on NAPA for reliability and breadth. In the eyes of many, the brand’s resilience has proven durable even when other aspects of the business cycle have shown volatility. The 2024 and 2025 periods provided a canvas on which leadership could demonstrate that the company could sustain growth while navigating supply chain dynamics, digital modernization, and a shifting competitive landscape. The emphasis on independence is not a symptom of weakness; it is a strategic bet that focusing resources on a single, mission-critical enterprise will yield superior outcomes over time. If the broader market can tolerate a period of transition, the long-horizon appeal of a specialized, well-capitalized automotive parts chain becomes increasingly compelling.

From a customer and partner perspective, continuity remains the operating compass. The networks that customers rely on—the brick-and-mortar stores, the distribution centers, and the AutoCare ecosystem—are not being dismantled or retracted. Instead, they are being reinforced with a clearer strategic owner and a firmer investment thesis. The news of a split invites questions about how everyday operations will function during the transition. Importantly, the aim is to preserve the cultural and logistical strengths that have built trust with repair shops, independent retailers, fleets, and DIY enthusiasts. A separate, more nimble corporate entity can also accelerate investments in inventory management, supplier relationships, and digital platforms that customers use to locate parts, check availability, or arrange service workflows.

It is also necessary to acknowledge that public sentiment around large employers often carries complexities unrelated to strategic direction. Some employee feedback surfaced in late 2025, with reviews on wage levels and management styles reflecting internal workplace concerns rather than systemic threats to the business’s viability. While these voices matter—hiring practices, wage competitiveness, and culture shape performance in the long run—the immediate health of the company, as measured by revenue, market presence, and the structural mechanisms of the split, points toward continued operations and expansion possibilities. The business challenges voiced by employees are real and merit attention, but they do not negate the fact that the company remains a sizeable, influential participant in the North American automotive aftermarket. The split is not a retreat from people or process; it is a bet that two focused, well-capitalized leaders can do more for employees, customers, and suppliers when they operate without the crosscurrents of a broader conglomerate.

The public record also notes a 2024 period during which digital tools, including mobile and web experiences, faced some friction—specifically around inventory accuracy. Such issues are not unusual for a large, distributed retailer coordinating wide supplier networks and complex logistics. They are reflection points, not existential threats. In the context of a major corporate realignment, they become priorities for remediation and enhancement rather than excuses for concern. The transition plan explicitly includes investments in technology, data governance, and omnichannel capabilities that should improve inventory visibility, order accuracy, and speed of fulfillment. When a company with a vast footprint commits to upgrading its digital spine, it signals a serious intent to stay ahead of customer expectations and to strengthen the reliability that underpins everyday commerce. Taken together, these strands—robust 2025 performance, a sprawling store and service network, investor-driven strategic clarity, and a disciplined plan to modernize operations—create a narrative of expansion rather than endgame.

For readers tracking the health of the company, the key takeaway is that the business is not shrinking into a controlled wind-down. It is reorganizing to harness scale with precision, separating the parts of the operation that most benefit from independent governance and capital discipline. The split is designed to yield two entities with stronger strategies, healthier balance sheets, and clearer alignment to the markets they serve. In the case of the automotive parts and service line, that means a sharper focus on supply reliability, service ecosystems, and the kind of customer experience that keeps repair shops and DIYers returning. For the market at large, this strategic move communicates confidence in the long-term viability of a foundational player in the aftermarket—an entity large enough to warrant careful scrutiny, yet disciplined enough to adapt to a rapidly evolving landscape.

The implications for the broader ecosystem are nuanced. Suppliers, independent garages, fleet operators, and end consumers all benefit when a dominant distributor can invest more aggressively in product availability, service capabilities, and digital tools that reduce friction in purchasing and repair workflows. A split structure can also create clearer governance for capital allocation, allowing each new company to pursue acquisitions, partnerships, or product development programs that align with its defined mission. While the future remains to be written in detail as the new corporate pages take shape and the stock market begins to price the new entities, the current trajectory is unmistakably constructive. The automotive parts distribution space is intensely competitive, and the ability to double down on core competencies while shedding non-essential complexity is precisely the kind of strategic maneuver that can translate into stronger market position over time.

In this moment, the central question shifts from whether the business will endure to how it will evolve. The answer, grounded in the February 2026 boardroom decision and the credible performance metrics that preceded it, is that NAPA is not retreating from the field. It is choosing to play a longer, more specialized game with greater clarity of purpose and a more targeted set of goals. The new organizational architecture—two independent, publicly traded entities—can be a powerful mechanism to deliver sustained growth, improved efficiency, and a more precise alignment between management incentives and the outcomes customers and shareholders expect. For analysts, customers, and industry observers, the message is clear: this is a moment of renewal, not retreat. The company’s scale, its nationwide reach, and its enduring relevance to the aftermarket create a foundation upon which careful, intentional growth can be built. The coming years will reveal how effectively the split translates into faster decision-making, smarter capital allocation, and a more responsive, customer-centric operation. What remains certain is that the organization is taking deliberate steps to sharpen its edge, and that, in the long arc of the market, dependability and strategic clarity often translate into enduring resilience.

null

null

Stability in a Shifting Aftermarket: Reading Customer Feedback and Service Continuity for the National Auto Parts Chain

Public information as of early 2026 presents a clear, if nuanced, portrait of a national auto parts chain that remains firmly in operation. The company behind one of the most expansive networks of parts stores in the United States is not reported to be in bankruptcy or preparing to exit the market. It sits within a long-standing publicly traded parent company known for a diversified portfolio of automotive aftermarket businesses, a structure that provides capital access, procurement leverage, and a broad ecosystem of suppliers and customers. What the public and industry observers emphasize is not a crisis of solvency, but a steady, ongoing process of adaptation to a rapidly evolving retail landscape. In short, the chain is actively pursuing strategies to preserve service continuity even as the competitive environment around auto parts continues to tilt toward digital channels, third‑party marketplaces, and heightened expectations from professional shops and DIY customers alike. This broader context matters because the question of “going out of business” hinges less on isolated store closures and more on how a retailer preserves reliability, inventory accuracy, and consistent service across thousands of storefronts and digital touchpoints.

The corporate frame around the chain helps explain why, despite a loud chorus of internal complaints that often appears on employment review platforms, the business itself has not shown signs of systemic distress. Public commentary about wages, management styles, or worker experience, such as concerns voiced in late 2025, points to internal management challenges typical of large organizations. These issues, while serious for employees and potentially affecting morale and day-to-day operations at specific locations, do not in themselves signal a strategic or existential threat to the company’s ability to serve customers nationally. In this light, the public record suggests a distinction between workplace sentiment and corporate viability. The broader enterprise—anchored by decades of industry experience, extensive supplier relationships, and a diversified revenue footprint—continues to be treated by investors and analysts as a durable platform rather than a fragile entity.

From the customer’s vantage point, the most salient evidence of continuity lies in ongoing store traffic, service capacity, and the ability to fulfill parts in a timely manner. A consumer survey referenced in industry chatter from September 2024 highlighted a friction point: a mobile app that occasionally struggled with inventory accuracy. Yet even with this flaw, shoppers indicated they would persist with the retailer because the network’s physical footprint—its local stores staffed by knowledgeable personnel and its accessible pickup options—remained a dependable channel for acquiring parts. That mix of brick-and-mortar and digital capability is precisely what keeps a retailer in the competitive loop. It is also a reminder that in the automotive aftermarket, people and local expertise matter as much as price and assortment. When a customer calls a store to confirm an obscure part, or when a technician needs a quick recommendation on a hard-to-find catalog number, the value of a strong physical presence cannot be overstated. The chain’s response to inventory challenges, therefore, becomes less about erasing every hiccup and more about delivering consistent, reliable service across channels, a signal that the business is focused on continuity rather than retreat.

The automotive aftermarket has entered a period of rapid digital metamorphosis. Traditional players, once defined by their store networks and counter salesmanship, now compete with e-commerce platforms and catalog-driven retailers that push fast shipping, transparent pricing, and expansive online catalogs. In this environment, a retailer with a long, deep footprint is well positioned to weather disruption because it can blend digital convenience with hands-on support. The current strategic emphasis appears to center on strengthening digital interfaces—inventory visibility, order status updates, and cross-channel fulfillment—while maintaining the trusted service guarantees that customers associate with a physical storefront. The synergy between online capabilities and the human touch in-store can transform a potential weakness—inventory inaccuracy on a screen—into an opportunity to reframe the shopping experience as a partnership between digital tools and human expertise. The net effect is a more resilient operation that preserves service continuity even as the shopping journey shifts toward online discovery and offline pickup.

Industry observers also note that the long-term health of any large auto parts retailer depends on a balanced approach to growth and capital allocation. The enterprise in question sits within a parent company with a long public track record, a history of capital markets access, and a diversified product and supplier base. That foundation matters because it underpins ongoing investments in supply chain resilience, warehouse automation, and data analytics that can compensate for the kinds of inventory misalignments that sometimes surface in consumer-facing apps. When a retailer can allocate capital to improve forecasting, diversify supplier relationships, and modernize its stores, it reduces the risk of cascading problems that might otherwise threaten continuity. In this sense, the absence of bankruptcy or orderly exit signals in the public domain becomes a meaningful indicator of the organization’s capacity to weather sector-wide shifts. The question of whether the chain will endure is less about a single year’s earnings and more about the durability of its operating model, its capital structure, and its capacity to adapt to evolving consumer expectations without sacrificing reliability.

A key thread in this discussion is how the chain communicates with and supports its diverse customer base. The aftermarket serves two broad constituencies: professional automotive technicians and do-it-yourself enthusiasts. Each group has distinct needs, yet both expect accuracy, speed, and reliability. When a customer turns to a store for a difficult-to-find component, they rely on staff who grasp the nuances of fitment, compatibility, and warranty coverage. When a DIY shopper uses an online catalog, they expect the same level of accuracy and the option for fast pickup or reliable shipping. The chain’s ongoing digital transformation is not merely about presenting a sleek storefront online; it is about ensuring that inventory data across physical and digital channels is coherent and trustworthy. The news of app shortcomings in 2024 should be viewed in this light—as a solvable interface problem within a larger system that still delivers everyday value to a broad customer base. The capacity to fix those problems, communicate clearly about service expectations, and maintain cross-channel reliability forms the backbone of ongoing continuity, which is precisely what customers rely on when they decide where to purchase parts.

For readers seeking a practical sense of how an industry-leading retailer sustains continuity amid disruption, consider the broader ecosystem in which the chain operates. A single, tangible example of the kind of online-to-offline integration customers expect can be found in specialized parts catalogs and their cross-referencing logic. In some corners of the aftermarket, even a well-regarded online catalog can stumble when a part’s cross-reference is complex or the catalog entry fails to reflect updated supplier information. The way a retailer handles such gaps often reveals more about resilience than a spotless year of sales. A nod to this dynamic appears in the sharing of catalog pages from niche shops that show how professional buyers navigate the same challenges—accurate fitment, availability, pricing, and lead times. While these site-specific examples come from a different segment of the market, they signal a universal truth: continuity hinges on robust data, transparent communication, and a willingness to invest in both human and technological capital.

In this context, the chain’s public posture—emphasizing ongoing operations and a digital-first but service-forward strategy—reads as a cautious optimism rather than complacency. It implies a belief that the market will continue to value a dependable network that can fulfill both the immediate needs of a repair job and the long-tail requirements of enthusiasts chasing rare or discontinued parts. The dynamic tension between digital optimization and human expertise is not a sign of weakness but rather the essential engine of evolution in the aftermarket. When the chain negotiates that tension well, customers experience continuity that transcends the occasional misstep in the app or the occasional staffing challenge at a single store. And when that continuity is felt consistently across regions and channels, the business earns a degree of trust that is hard to replicate in a purely online or purely in-store model.

From a reader’s perspective, these dynamics matter because they shape expectations. If the public record shows no imminent threat of closure or bankruptcy, the question becomes not whether the chain will survive, but how it will continue to thrive in a more competitive, more digitally oriented environment. The answer lies in the ability to blend a broad, efficient supply network with an enhanced, user-friendly digital experience, all while sustaining the local relationships that are the hallmark of brick-and-mortar retail in this sector. The industry’s trend lines suggest that the future belongs to retailers who can offer convenience without sacrificing the expertise and accountability that technicians and serious DIYers rely upon. In other words, continuity is not about preserving the status quo; it is about executing a deliberate transformation that preserves service levels in the face of changing consumer preferences and increasing marketplace volatility. And that, in turn, strengthens the case that the chain remains a durable player in the North American aftermarket.

As a practical reflection for readers who want to connect the dots between feedback, operations, and viability, consider how a large retailer absorbs and responds to customer and employee signals without compromising service continuity. Employee concerns about wages or management practices highlight areas for internal reform that can improve morale and performance, especially at the store level where customer contact happens. Meanwhile, customer feedback about app inventory and catalog accuracy underscores the ongoing need for better data governance, more precise fulfillment, and clear communication about stock status and alternatives. Taken together, these signals point to a company in a phase of deliberate adjustment rather than a company in decline. The real measure of stability will be the chain’s ability to translate feedback into tangible improvements across stores and across digital channels, ensuring that customers can reliably source the parts they need, when they need them, through whichever channel they prefer. In this sense, continuity is both a state of operation and a continuous process of improvement.

For readers who want a tangible touchstone beyond narrative assessment, a related example from the broader auto-parts ecosystem serves as a reminder that the aftermarket is not monolithic. It shows how cross-channel challenges can be managed when data, logistics, and customer service are treated as a unified system rather than as disconnected silos. The practical upshot for the national chain is simple: invest in the alignment of inventory data across storefronts and online catalogs, empower store teams with the knowledge to resolve difficult fitment questions, and maintain a flexible logistics approach that can flex with demand surges and supply disruptions. These commitments are the kind of systemic actions that reinforce service continuity and, by extension, the retailer’s ongoing presence in the market. In this environment, the absence of bankruptcy rumors or market exit signals is not a marker of complacency; it is an indicator that the organization remains capable of orchestrating a complex set of capabilities to keep customers connected to the parts they need.

To illustrate a concrete takeaway for readers, consider how cross-disciplinary capabilities—data analytics, supply chain optimization, and frontline expertise—must work together. When they do, the experience for the consumer becomes less about chasing a part and more about receiving timely, accurate guidance and a solution that keeps a repair on track. The chain’s continued operation and its commitment to digital modernization, coupled with its extensive physical network, suggest a model of resilience that many in the industry will study as the market continues to evolve. If there is a cautionary note, it lies in acknowledging that the path of transformation is never linear. Customer expectations can evolve quickly, and employee sentiment can shift with labor market conditions. The challenge is to translate those shifts into measurable improvements—fewer inventory discrepancies, faster fulfillment, clearer communication, and a culture that aligns frontline service with the strategic priorities of the enterprise.

In closing, the evidence at hand supports a cautious but confident view: the major national auto parts chain remains a durable player within a competitive field. It is not immune to the pressures that affect all large retailers—rising digital expectations, the allure of third-party marketplaces, and the ever-present need to manage inventory with precision. Yet the combination of a strong corporate backbone, an expansive store network, and an ongoing digital transformation program gives the business the levers it needs to maintain continuity. The absence of explicit signals of exit or bankruptcy signals that the chain is prioritizing a pragmatic, long-term path rather than short-run expediency. For customers and industry observers alike, that means continuity in service—even as the market reshapes itself around new modes of shopping and new expectations for speed, accuracy, and convenience.

03-06 Mitsubishi Evolution 8-9 JDM rear bumper OEM

External resource: https://www.gpc.com/investor-relations

A Strategic Split, Not a Shutdown: What a Corporate Restructure Means for NAPA Auto Parts and the Aftermarket

When a corporate giant announces a major structural pivot, the natural reflex is to scan for signs of trouble. Yet the February 2026 restructuring unveiled by Genuine Parts Company (GPC) presents a different narrative. Rather than signaling a retreat from the market, the move is framed as a decisive pivot toward greater focus, speed, and capital allocation. It marks a deliberate separation of two core businesses into independent publicly traded entities. Within that framework, the automotive parts division, which houses the NAPA brand, emerges not as a candidate for decline but as a cornerstone of a long‑term growth plan. The underlying message is clear: management believes the value of each business is best realized when it can pursue its own growth strategy with tailored resources, governance, and investor mandates. In this light, the question “Is NAPA going out of business?” gives way to a different inquiry—what does a strategically guided spin‑off mean for customers, employees, supply partners, and the competitive landscape of the automotive aftermarket over the next five to ten years? The answer, based on the most current information, is that NAPA is positioned to thrive through a new phase of focused investment and market agility rather than fade into the background of a consolidating industry.

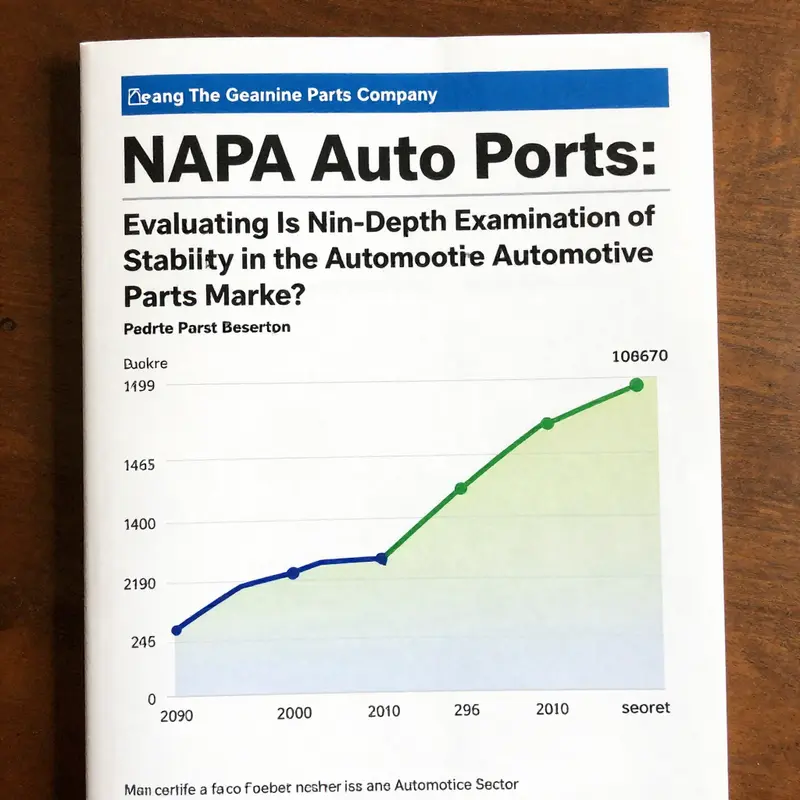

To appreciate the significance, one must first map the structure and rationale of the move. GPC’s plan calls for splitting its two core businesses into separate, independently traded companies. For the automotive parts division, this separation is described as a liberation from overhangs that can accrue when two distinct strategic priorities share the same corporate umbrella. The automotive‑parts ecosystem—NAPA among its most esteemed brands—operates with a footprint that spans stores in 17 countries and a network that serves both retail customers and professional repair ecosystems. The scale is considerable. Industry conversations and the disclosed guidance point to sales in the vicinity of over $150 billion annually for the automotive parts division, underscoring the division’s central role in the global aftermarket. Such scale is not incidental; it reflects decades of investment in supplier relationships, distribution infrastructure, and a service model rooted in reliability and breadth of inventory. The spin‑off framework is designed to unlock that scale for independent strategic oversight, enabling management to tailor capital allocation, partnerships, and growth accelerants without competing with a sister business for attention or resources.

The financial architecture accompanying the spin‑off also speaks to a long‑term confidence in NAPA’s trajectory. Even as the announcement presented a disappointment on quarterly earnings—an atmosphere not uncommon when one major corporate structure pivots—the broader calculus remains unaltered: the underlying business is strong, resilient, and positioned to capitalize on favorable secular trends. The executives and their financial advisers, including top‑tier firms, emphasize that the split is about unlocking value and enabling specialized growth trajectories. In markets where investors increasingly reward management teams that can demonstrate clear, autonomous paths to capital deployment, the spin‑off is a signal of intent rather than an alarm about viability. For stakeholders monitoring the health of the auto parts ecosystem, this move is a reminder that strategic clarity can be as valuable as earnings surprises in the near term. The prudent takeaway is not to equate short‑term headline misses with long‑term fragility.

From a broader industry perspective, the reshaped GPC portfolio suggests two parallel dynamics. First, the automotive parts segment retains its central role as a high‑demand, durable‑goods business anchored in replacement parts driven by aging vehicles and ongoing maintenance needs. Second, the market’s appetite for focused growth vehicles—entities that can concentrate investment and innovation on specific customer segments—remains robust. In practice, the spin‑off provides the automotive division with greater capital flexibility to pursue technology adoption, supply chain modernization, and store network optimization without needing consensus across unrelated divisions. For a customer base that spans DIY enthusiasts, professional technicians, and fleet operators, the structural change should translate into steadier product availability, more reliable service, and continuous improvements in the buying experience. The sheer scale—over $200 billion in market capitalization for the parent entity and a similar magnitude of influence in the aftermarket—gives NAPA a durable platform from which to negotiate with suppliers, financiers, and logistics partners. The market’s reaction to the plan was a temporary dip on earnings news, but the longer arc suggests a re‑rating toward a more precise, growth‑oriented narrative about what the business can achieve when unshackled from broader corporate constraints.

The narrative around customers and operations is equally important. NAPA has long been a national brand with a widespread footprint and a reputation for breadth and reliability. The spin‑off does not alter the basic mechanics of how customers access parts, nor does it immediately jeopardize the stability of the supply chain. The realignment is designed to preserve continuity while accelerating improvements. In practical terms, customers should expect the same store network, the same procurement channels, and the same ability to rely on local knowledge and fast part availability. Of course, there can be an adjustment period as separate governance processes take hold and as each entity optimizes its internal systems. Yet the strategic intent is to build a more nimble, customer‑centric organization. The ecosystem will continue to rely on a deep, well‑cushioned supplier base and a distribution backbone engineered to meet the needs of both walk‑in retailers and professional customers who demand speed and accuracy.

The recent public narrative also recorded some employee feedback that has occasionally surfaced in public forums. While there have been complaints about wages and management styles, these voices reflect the realities of day‑to‑day work life rather than an existential threat to the business model. In large, mature corporations, such concerns are not unusual, especially during periods of rapid organizational change. The broader signal remains unaltered: the company remains a major employer and a critical part of the North American aftermarket. The spin‑off does not imply a retreat from employment commitments; it signals a reallocation of resources and a reimagining of career pathways that could eventually yield clearer reporting lines, greater accountability, and new opportunities for professional development as the organization grows in its newly defined independent form.

The strategic logic of the split is reinforced by the external financial optics that accompany such moves. Investors have grown accustomed to structures that can optimize capital allocation by reducing corporate complexity. A separation can unlock value by enabling each entity to pursue growth strategies aligned with its own business model, risk profile, and capital needs. For NAPA, that means an opportunity to sharpen its focus on the aftermarket’s core drivers—replacing aging components, meeting the needs of aging fleets, and strengthening the repair network that underpins vehicle reliability. It also means the chance to accelerate modernization initiatives—such as inventory accuracy, data analytics, and omnichannel capabilities—that can deliver a more seamless customer experience, especially for busy professionals who depend on fast, accurate service across a broad network. The emphasis on investment and strategic autonomy is a good sign for those who follow the industry closely, as it suggests management is prioritizing long‑term value creation over quarterly beats that may be difficult to sustain in a rapidly evolving market.

To be sure, the road ahead will involve challenges as the two new entities mature. The automotive division will navigate the usual tensions of growth—how to balance investment with cash flow, how to manage supplier relationships in a highly competitive environment, and how to translate strategic initiatives into tangible improvements in stores and online channels. The cross‑functional coordination that previously benefited from shared leadership will now occur across corporate boundaries, which can slow certain initiatives at first. But the absence of distress signals, combined with a structurally leaner and more agile framework, offers a clearer path to execution. The company’s public disclosures stress that the spin‑off is designed to unlock value and to enable faster, more disciplined deployment of capital where it matters most for the automotive business. In an industry where the pace of change—from e‑commerce to supply chain digitization and parts localization—has accelerated, the ability to deploy capital quickly in response to market developments is a meaningful competitive edge.

From a risk perspective, observers should differentiate between near‑term volatility and long‑term viability. The earnings miss accompanying the restructuring reflects, in part, typical transitional costs and the normalization of a changed corporate governance structure. It does not necessarily portend weaker demand for parts or a shrinking customer base. In fact, the demographic trends—an aging vehicle fleet, increasing vehicle mileage, and ongoing investment in maintenance—remain supportive of sustained demand. The aftermarket’s resilience is anchored in necessity: vehicles will still need parts, and the repair network will still rely on a broad, reliable supply. The spin‑off could even strengthen resilience by allowing each business to tailor its risk management practices, supplier diversification, and capital strategies to its own operating realities. In such a framework, the risk of a sudden, systemic downturn affecting both entities at once is mitigated by the clarity of separate strategies and the discipline of independent governance.

The macro context further reinforces a cautious optimism. While some segments of the auto retail landscape have seen shifts in market leadership—some peers report changes in store performance and margins—the automotive parts division remains a central pillar of the North American aftermarket. The structural tailwinds—replacement demand driven by aging vehicles, the growth of professional repair work, and the increasing complexity of vehicles requiring specialized parts—likely to persist. The spin‑off is therefore less about a temporary rebound and more about aligning capabilities with the demands of a modern, digitized, and increasingly service‑oriented aftermarket. In this sense, the move resembles a strategic repositioning rather than a retreat. It invites observers to watch not only the top‑line performance but the quality of execution, the speed with which the new independent entity can implement its growth plan, and the ability of the broader ecosystem to adapt to a more focused, capital‑efficient model.

For stakeholders, the practical implications of the restructuring are worth noting. Customers can expect continuity in service and continued access to a comprehensive parts assortment, supported by a distribution network designed for reliability. Suppliers can anticipate a single‑mized channel for collaboration, potentially unlocking more direct engagement with the automotive division as an independent growth engine. Franchisees and independent store operators will be keenly watching how governance and capital allocation evolve, especially in relation to store modernization programs, inventory management, and digital investments that bridge the physical and online experience. In a market where competition remains intense, the capacity to tailor operations to local demand while maintaining scale is a distinct advantage. The growth potential behind the spin‑off is rooted in the aftermarket’s fundamental need to keep vehicles on the road—an enduring driver that transcends quarterly results and market cycles.

In sum, as of February 20, 2026, the question is not whether NAPA is going out of business, but how a carefully executed corporate transformation will shape its future. The restructuring signals confidence in the long‑term viability and strategic value of the automotive parts division. It reflects a prudent allocation of resources, a commitment to capital efficiency, and a willingness to embrace a more agile governance model. For customers, employees, investors, and partners, the message is clear: the brand remains a central, enduring fixture of the aftermarket, with a defined path to growth that is not contingent on the survival of a single corporate umbrella but on the execution of a focused strategy. The road ahead will require patience and disciplined management, but the foundation is solid, and the market fundamentals remain favorable. In an industry that rewards resilience, adaptability, and scale, NAPA’s trajectory after the spin‑off will likely be determined by how well the new independent entity translates strategic intent into tangible value for its customers and partners over the coming years.

Final thoughts

In summary, the operational outlook for NAPA Auto Parts thankfully reveals no imminent closure or bankruptcy threats. While employee sentiment indicates some internal challenges that need addressing, the overall financial health remains robust. Customer feedback shows a willingness to continue utilizing services despite minor issues. By carefully analyzing these multifaceted aspects, it is clear that NAPA Auto Parts is not only surviving but also strategically positioned in the automotive aftermarket, much to the reassurance of its business stakeholders.